(more…)

(more…)

We have run out of superlatives to describe the greater Toronto residential resale marketplace. Records have been broken consistently for the last few months, and September was no exception. Two records were shattered in September: most sales ever recorded for the month, and the highest average sale price for all properties reported sold.

(more…)

July’s residential resale market performance was record breaking. Almost 11,100 properties were reported sold, a 28 percent increase compared to the 8,679 properties sold a month earlier. Compared to July 2019, sales improved by almost 30 percent. There were 8,555 residential properties reported sold last year. July’s numbers are the clearest indication as to the robustness and resilience of the Toronto marketplace, especially when fueled by record-low mortgage interest rates.

(more…)

By any standards, the residential resale market’s recovery in June was nothing but phenomenal. The lockdown and emergency measures implemented by the Province in mid-March literally brought the market to a standstill. It stayed that way throughout April, but by early May, we could sense recovery. By May the industry, agents, buyers and sellers had adjusted to the rigid in-person showing protocols – masks, gloves, sanitizers, social distancing, and no-touch viewings. Also, by May, the pent up demand, already present before the pandemic, began to push against the restrictions imposed by Covid-19 and sales began to take place.

(more…)

The Toronto and area resale market performed as expected in April. As reported in our March report, the implementation of the emergency lockdown measures had a crushing impact on the resale housing market. With most businesses closed and more than three million Canadians unemployed there was no reason to believe that the resale market would miraculously revive in April.

Until the Ontario Provincial Government declared a state of emergency, the Toronto and area residential resale market was on course to produce one of the strongest, most robust markets on record, including the establishment of a record-breaking monthly average sale price. All that changed around the middle of the month as people began following provincial health authorities directives: stay home, maintain social distancing, no large gatherings, and of course, wash your hands frequently. When many of Ontario’s businesses were ordered closed, the real estate market didn’t stop but stalled dramatically. (more…)

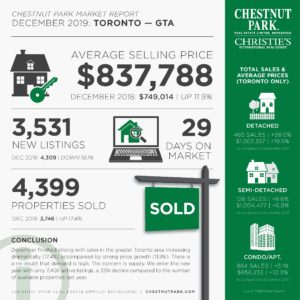

The December market for residential resale properties came in exactly as anticipated, with substantially higher sales and average sale prices compared to last December, and not surprisingly, the month and year ended with a critical shortage in available resale inventory.

In December 4,399 properties were reported sold. This is not a record high for the month, but these sales represented more than a 17 percent increase compared to the 3,746 properties reported sold last December. Past Decembers have seen more properties sold during the month, but the 4,399 properties that were sold was a very healthy recovery from last year’s dismal results.

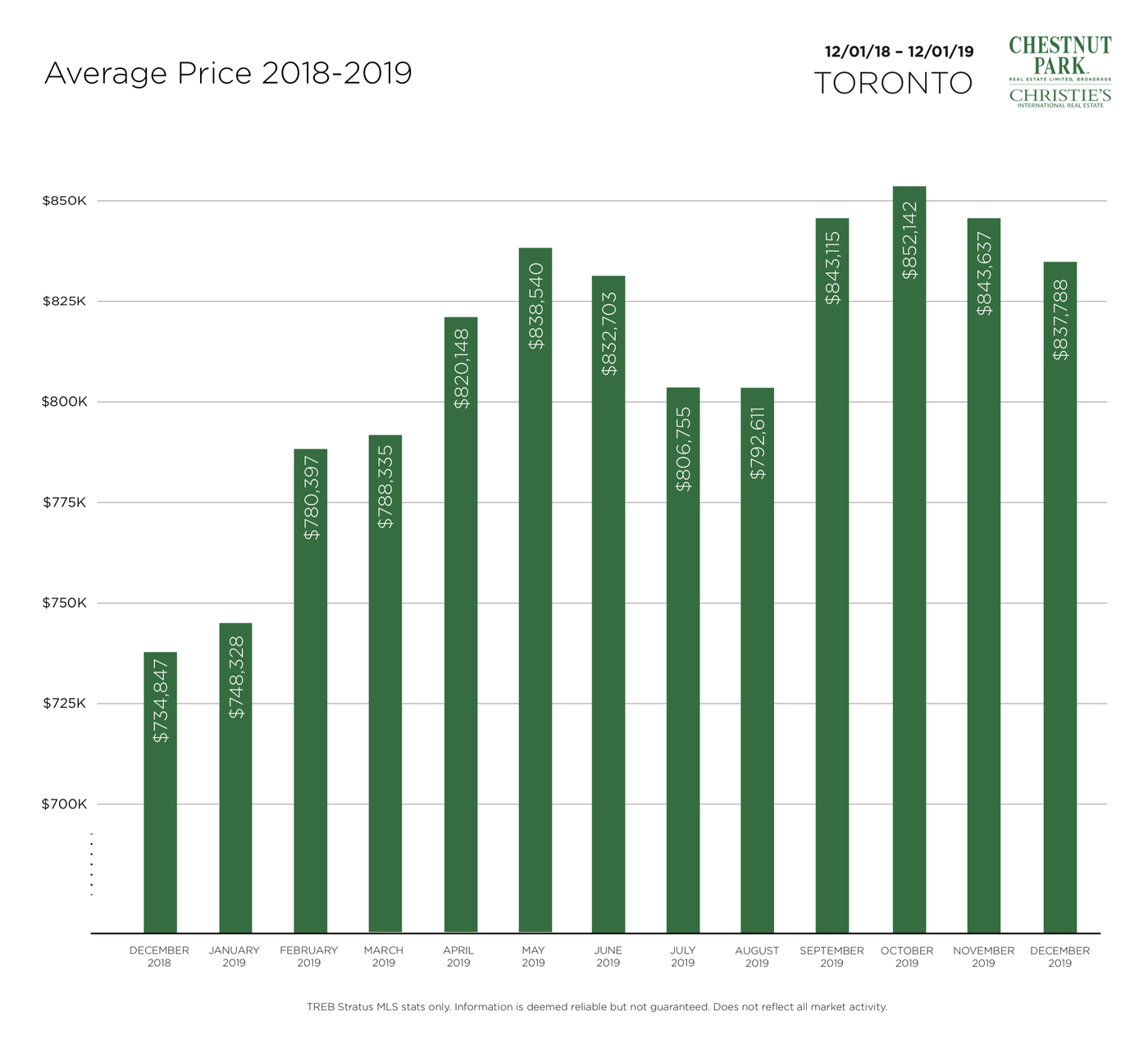

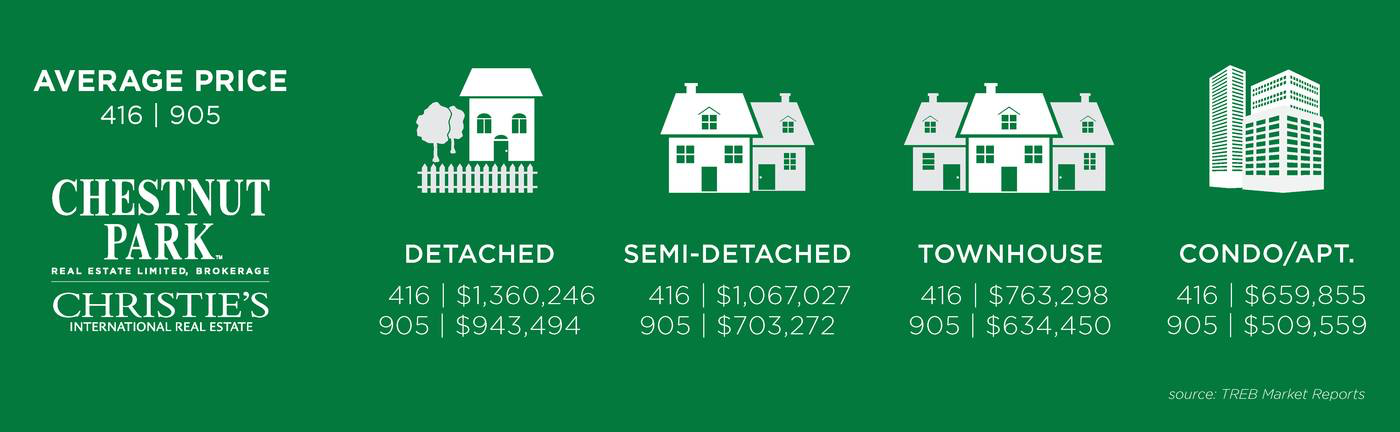

The average sale price for all properties sold in the Greater Toronto Area came in at $837,788, almost 12 percent higher than the average sale price of $749,014 achieved last year. Homeowners will no doubt be happy with this increase, but the rapidly rising prices, once again approaching record levels, put a strain on affordability and their longer-term sustainability, especially with salaries and wages increasing by about 3 percent annually.

The average sale price in the City of Toronto was even higher coming in at $885,132, an exceptionally high number for the month of December when sales of higher-priced properties decline. This increase was driven by the sale of 465 detached properties sales having an average sale price of $1,363,477, a 19.5 percent increase compared to the number of detached properties that were reported sold in December of 2018.

On a yearly basis, 87,825 residential resale properties were reported sold. This represents a strong 12 percent recovery compared to the 78,015 properties reported sold for 2018. Compared to recent resale history, 2019’s results are still weak. In 2014, 92,782 properties were reported sold. That number jumped to 101,213 in 2015 and then to 113,040 in 2016, before dropping to 92,335 in 2017. The 113,040 properties sold in 2016 remains the record high for Toronto and area sales.

Notwithstanding rising resale prices, 2019 sales results might have been higher had there been more inventory for consumers to buy. Housing data related to inventory at the end of December is seriously concerning.

In December 3,531 new properties came to market. That compares poorly with the 4,309 that came to the market last December. Unfortunately, we witnessed inventory declines throughout 2019. As a result, at the end of the year, there were only 7,406 properties available to potential buyers, a stunning 35 percent decline compared to the 11,431 properties available at the end of 2018. In some trading areas the situation has gone beyond critical. For example: in all of Toronto’s eastern trading areas 49 semi-detached properties were reported sold. At the end of December and heading into 2020 here were only 7 detached properties available to potential buyers. These are unprecedented low numbers. At the end of the year, there were no semi-detached properties available in Toronto’s popular eastern trading areas: Riverdale, Leslieville, and the Beaches.

The inventory shortage has also spread to Toronto’s condominium apartment sector. In December 844 condominium apartments were sold in the City of Toronto. During the same period, only 779 new condominium apartment listings came to market, clearly far less than the overwhelming demand. As for the end of December, there were only 1,148 condominium apartments for sale in the City of Toronto – based on December’s sales that is just 1.2 months of inventory.

Year-end numbers indicate that inventory will play a crucial role in the success of the Toronto area residential resale market in 2020. If sellers decide to take advantage of the near-record sale prices and bring their properties to market, Toronto’s residential resale market will be strong and produce year-end sales that exceed the 87,825 properties that were reported sold this year. Price appreciation should be muted by the fact the average prices are at record highs and restrained from further growth by affordability.

Prepared by Chris Kapches, President and CEO

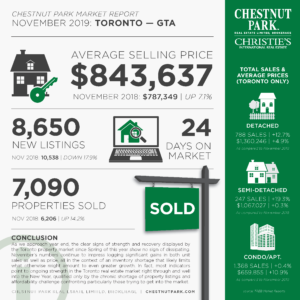

The November market report has basically written itself. It is another month with results almost identical to the preceding eight months. Sales were up substantially compared to November last year, and similarly average sale prices also rose.

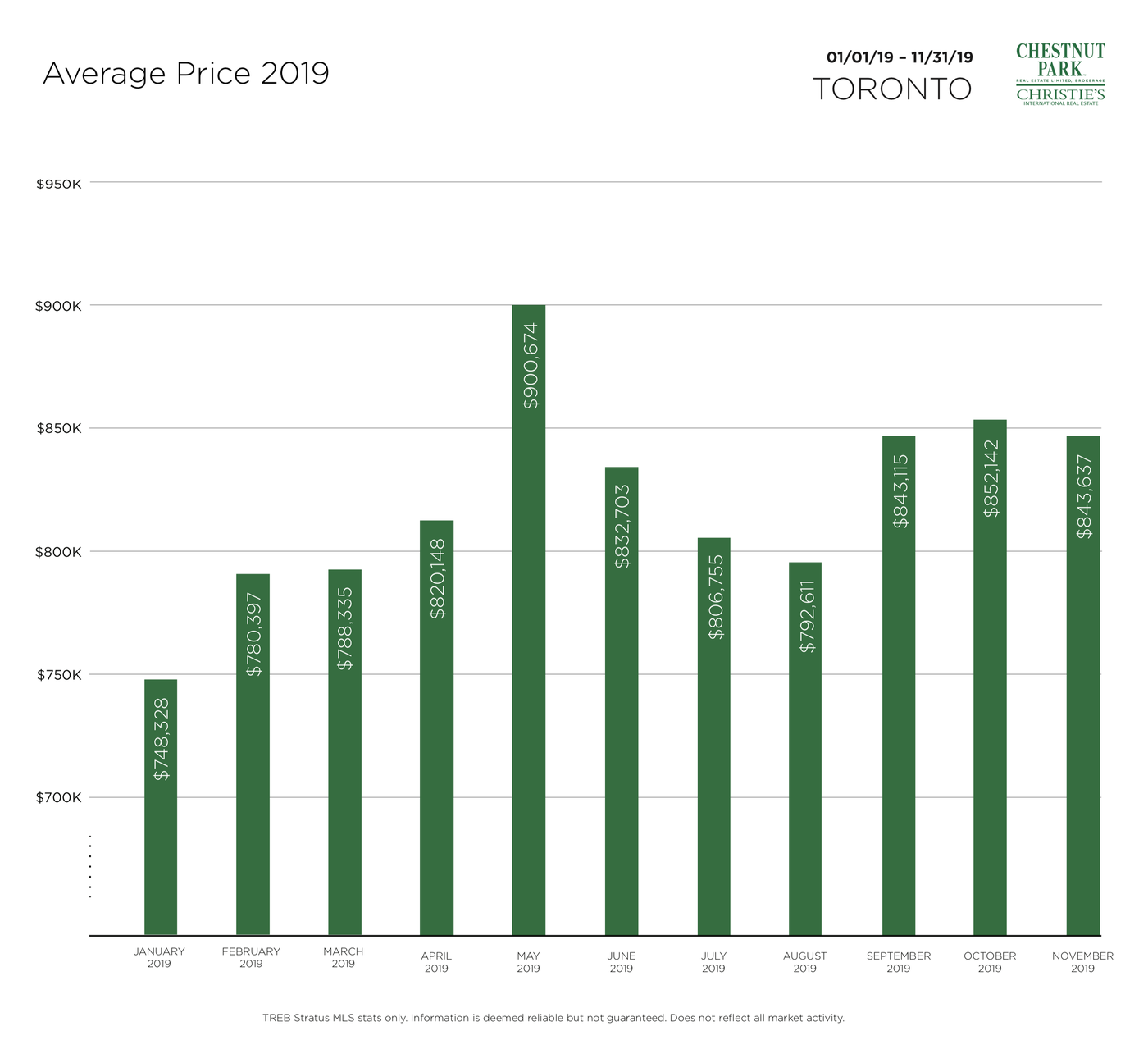

Specifically, sales rose by almost 15 percent compared to last year, from 6,206 to 7,090 this November. The average sale price rose over 7 percent, from $787,349 last year to $843,637 this November. These are greater Toronto and area numbers. In the City of Toronto the average sale price rose to a stunning $910,419. This number is stunning for two reasons: it includes all condominium apartment sales, and secondly, it is approaching the record high average sale price achieved in March 2017, before the implementation of the foreign buyers tax and the mortgage stress testing which took effect in January of 2018.

There are two stories that emerge in the November residential resale data. Firstly, the concern about supply. In November only 8,650 new properties came to market. This compares very poorly to the 10,538 that came to market last year, a shocking 18 percent decline. Even more concerning is the available supply as we move to the end of 2019. At the beginning of December there were only 11,958 properties available, in the entire greater Toronto area, for buyers to inspect and purchase. Last year, and this number was low, there were 16,420 available properties. That means the available inventory has declined by almost 30 percent on a year-over-year basis. On a months-of-inventory analysis, there are only 2.2 months of inventory for the greater Toronto area, and only 1.8 months for the City of Toronto. It is not surprising therefore that all properties that came to market in November sold in 24 days and for 99 percent of their asking price (100 percent in the City of Toronto).

The second story that immerges, and one much more positive than the first, is the resurgence of the 905 region residential marketplace. Following the implement of the foreign buyers tax in April 2017, the 905 region resale marketplace came to a standstill. It remained stagnant until the mid-point of this year, when signs of life appeared. Detached property sales rose by almost 28 percent in November, while townhouse sales increasedby almost 22 percent. Detached and townhouse property sales in the 905 region accounted for almost 50 percent of all sales achieved in the greater Toronto area in November.

Notwithstanding the surge in 905 region sales, average sale prices in the 905 region are still low compared to the City of Toronto.

As we head to the end of the year, demand in the greater Toronto area remains strong, even though average sale prices are approaching record highs. The concern is and will be supply. With only 11,958 residential properties available to buyers, all eyes will be on the new supply that comes to market in 2020. Hopefully the record average sale prices will cause sellers to capitalize on the strong alue of their properties, motivating them to bring them to market.

Happily, the Toronto and area residential resale market place delivered August results as anticipated and in a way that ensures that the resale market will remain stable, sustainable and accessible. The only concern is inventory, particularly in the City of Toronto.

Sales volumes were up by over 13 percent compared to August 2018, while the average sale price increased by 3.6 percent, right in line with the increase in wages. In August wages for permanent employees in Canada increased by 3.8 percent year-over-year. Considering that sales volumes are still playing “catch-up” from 2016 and 2017 numbers, a 13 percent increase compared to last year is modest.

In actual numbers 7,711 properties were reported sold in the greater Toronto area. Last year 6,797 were reported sold. The average sale price came in at $792,611 compared to $765,252 for the same period last year. It should be noted that the increase in sales volumes was concentrated in Toronto’s 905 region. Of the 7,711 reported sales 5,158 were primarily located in Halton, Peel, York, and Durham regions. Only 2,553 were City of Toronto properties. This number is almost identical to the 2,550 sales that took place in the City of Toronto last year. As these numbers indicate the City of Toronto made no contribution to the 13 percent increase in sale volumes across the entire marketplace.

The reason for this disparity is two fold. Firstly, the City of Toronto’s average sale price came in at $818,715, at least 5 percent higher than the average sale price achieved in the 905 region. More impactfully is the lack of inventory available to buyers in the City of Toronto.

Condominium apartment sales were practically flat in August (2.2 percent higher than last year). Condominium apartments have not only become pricey —— in the Central core of Toronto where most condominium apartments are located and sell, the average price is approximately $700,000. With mortgage stress testing a buyer of a condominium apartment would need household income substantially higher than $100,000 annually, and if their mortgage financing is high ratio at 10 percent equity, at least a $70,000 deposit. It is these factors that ultimately will keep average sale prices from increasing substantially more than 3 percent year-over-year for sometime to come, even if the Bank of Canada reduces its overnight lending rate, which its wisely refrained from doing at its meeting in early September.

Although condominium apartments are still selling briskly ——- all condominium apartment sales took place in 22 days (the rate in the overall market place was 25 days) and at 100 percent of their asking prices ——- inventory levels are down. Last year there were 2,307 active listing at the end of August. This year only 2,117. The same is true for the overall market. Last year there were 17,864 active listings available to buyers in the greater Toronto area, this year that number has dropped to 15,870, an 11.2 percent decline. This not good news for buyers, even those who have the financial means to comfortably afford Toronto real estate prices, a serious concern going forward.

The high end of the residential resale market also continued its slow recovery. In August 159 properties having a sale price of $2 Million or more were reported sold. Last year 144 were reported sold, an increase of 10 percent, a number that lags the over market place increase of 13.4 percent. As discussed in previous reports the average sale price of luxury properties out-distanced the overall market place in 2016 and early 2017. That sector of the marketplace is still correcting, however that process is now almost complete. In August the sale of detached properties (average sale of $1,246,392) increased by 0.3 percent compared to last year, one of the few year-over-year increases in the City of Toronto over the last few months.

Given some recent economic numbers there is nothing that would indicate that the prevailing resale market place will change throughout the remainder of 2019 and into 2020. As indicated above, wages rose by 3.8 percent in August; 81,100 new jobs were added to the Canadian economy, 23,900 of those being full-time jobs; and the Bank of Canada did not lower interest rates. If the Canadian economy continues to create jobs throughout the balance of 2019, we should make it to year-end with out the Bank of Canada reducing rates. All of this economic activity ensures a stable real estate market going forward, with modest increases in sale volumes and 3 to 3.5 percent increases in average sale prices.

Prepared by:

Chris Kapches, LLP, President and CEO, Broker

July marks the 5th consecutive month of recovery in the Toronto and area residential resale market place. It started in March with 7,138 reported sales. Since March there have been substantive positive monthly variances compared to 2018, culminating in July’s performance.

In July there were 8,595 reported sales, a dramatic 24.3 percent increase compared to the 6,916 sales that were reported in July of last year. Reduced mortgage stress testing thresholds, marginal declines in mortgage interest rates, a strong economy and growing consumer confidence are some of the factors responsible for this string of positive monthly results.

Another market positive is that we are seeing increases in the average sale price for homes in the greater Toronto area, but modest increases consistent with the rise in wages and the consumer price index. In July the average sale price came in at $806,755, only 3.2 percent higher than the average sale price of $781,918 achieved last July. This is the forth connective month where increases on a year-over-year basis have averaged about 3 percent. These increases are very encouraging because they ensure market stability and sustainability.

Market disparity between the Toronto market (416 region) and the greater Toronto area (905 region) continues, although it is not as extreme as it was in 2018 and early 2019. For example: the average sale price in the City of Toronto was $840,000, but only $807,000 in the greater Toronto area. The months of inventory in the City of Toronto is only 1.8 months, and 2.4 months in the 905 regions. All properties sold in the City of Toronto, including all condominium apartments, sold for 100 percent of their asking price (on average) and for only 99 percent in the 905 regions. Lastly in the City of Toronto all new listed properties spent only 20 days on market before being reported sold, while in the 905 regions they spent 23 days on the market. To repeat, although the disparity persists it is declining and not as marked as it once was.

The most sought-after housing type in the greater Toronto area are semi-detached properties. There was a startling increase of 42.3 percent in reported sales of semi-detached properties in the City of Toronto compared to similar sales in July 2018, although price growth was restrained at 5 percent. At months end there were only 257 semi-detached properties available for sale in Toronto. This is very problematic, since 276 semi-detached properties were reported sold in July, more than the total inventory of available properties in August. Unless a plethora of properties come to market in August and the fall, semi-detached properties will be like unicorns in Toronto’s resale marketplace.

The lack if inventory continues to be a concern for the greater Toronto market place. In July 14,393 new listings came to market, almost 4 percent more than the 13,873 that came to market in 2018. Unfortunately, due to the string of absorption numbers over the last four months – over 36,000 properties have been reported sold since March – we enter August with only 17,938 active listings, almost 10 percent less than the 19,725 listings that were available to buyers last year.

Average Home Price in Toronto

Although strong sales numbers were reported for detached properties in July – detached property sales were up by almost 30 percent compared to last year – average sale prices declined by almost 10 percent. Detached property prices are experiencing the whiplash effect. Leading up to April 2017 detached property values increased substantially higher than other property types. During 2019 there has been a downward pull on detached property values, bringing them in line with other housing types, correcting the pre-April 2017 run up.

As has been forecast in these reports for the past few months, the future of the Toronto and area residential resale market is clear – anticipate monthly increases in sales volumes of at least 10 percent and increases in the average sale price of about 3 percent compared to the same month last year. I do not believe that the fall election will have any significant impact on Toronto’s housing market and any stimulation that might be experienced by further declines in mortgage interest rates will be tempered by the mortgage stress tests that remain in place.

Prepared by:

Chris Kapches, LLB, President and CEO, Broker

Get in touch with us to explore your real estate goals and find the perfect property.

Contact Me